Dubai Real Estate Market Review: January 2026

Land transactions in January 2026 was 56.4% of the total transactions value. The market activity increased by AED 50 billion over January 2025, 92% YoY.

The Real Estate Report

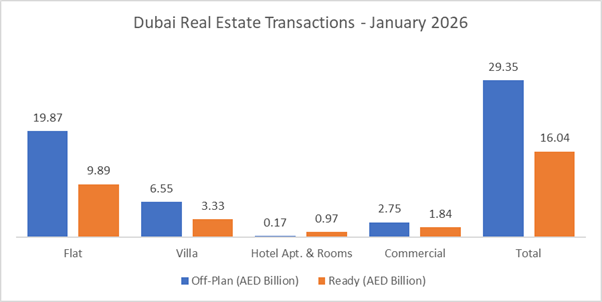

January 2026 closed with a total traded value of AED104.09B across 21,707 transactions, nearly double January 2025’s AED54.08B (+92.5% YoY). The month’s headline feature was Land, which accounted for the majority of value, while Off-Plan remained the strongest built-property engine by traded value.

| Category | Off-Plan (AED Billion) | Ready (AED Billion) |

| Flat | 19.87 | 9.89 |

| Villa | 6.55 | 3.33 |

| Hotel Apt. & Rooms | 0.17 | 0.97 |

| Commercial | 2.75 | 1.84 |

| Total | 29.35 | 16.04 |

Market Composition

| Segment | Value | Share of January Total |

| Off-Plan | AED29.35B | 28.2% |

| Ready | AED16.04B | 15.4% |

| Land | AED58.70B | 56.4% |

| Total | AED104.09B | 100% |

Off-Plan Market Performance

Total Off-Plan Value: AED29.35B (28.2% of the month)

Off-plan was led overwhelmingly by Flats, which made up over two-thirds of off-plan value.

| Category | Value | Share of Off-Plan |

| Flats | AED19.87B | 67.7% |

| Villas | AED6.55B | 22.3% |

| Commercial | AED2.75B | 9.4% |

| Hotel Apt. & Rooms | AED0.17B | 0.6% |

January’s off-plan market was essentially a flat-driven month, with villas a solid secondary pillar and commercial meaningful but clearly third. The highest ticket value for flats was Island 2 – AED80.0M, and for villas was The World – AED71.44M.

Top Performing Areas

| Area | Transactions |

| Damac Islands | 1,081 |

| Madinat Al Mataar | 672 |

| Dubai Islands | 648 |

| Dubai Land Residence Complex | 638 |

| Jumeirah Village Circle | 628 |

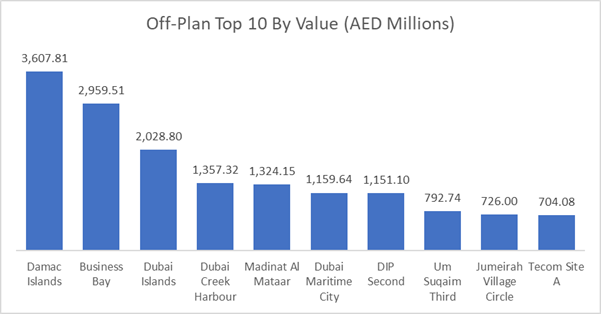

| Area | Value Traded (AED Billion) |

| Damac Islands | 3.61 |

| Business Bay | 2.96 |

| Dubai Islands | 2.03 |

| Dubai Creek Harbour | 1.36 |

| Madinat Al Mataar | 1.32 |

Ready Market Performance

Total Ready Value: AED16.04B (15.4% of the month)

Ready also skewed toward flats, but with a noticeably higher share for Hotel Apt. & Rooms versus off-plan.

| Category | Value | Share of Ready |

| Flats | AED9.89B | 61.7% |

| Villas | AED3.33B | 20.8% |

| Commercial | AED1.84B | 11.5% |

| Hotel Apt. & Rooms | AED0.97B | 6.0% |

Ready demand remained broad-based, with flats leading, and hotel/room product showing a more material footprint than in off-plan. The highest ticket value for flats was Jumeirah Bay – AED71.90M,and for villas was Palm Jumeirah – AED220.0M.

Top Performing Areas

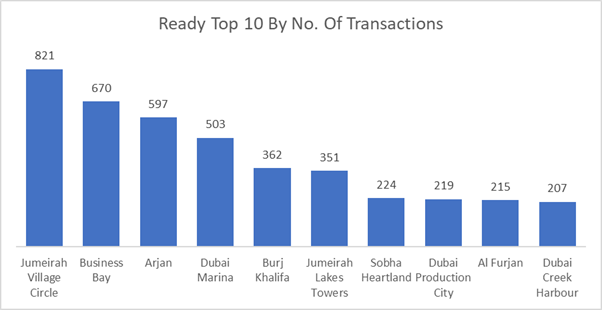

| Area | Transactions |

| Jumeirah Village Circle | 821 |

| Business Bay | 670 |

| Arjan | 597 |

| Dubai Marina | 503 |

| Burj Khalifa | 362 |

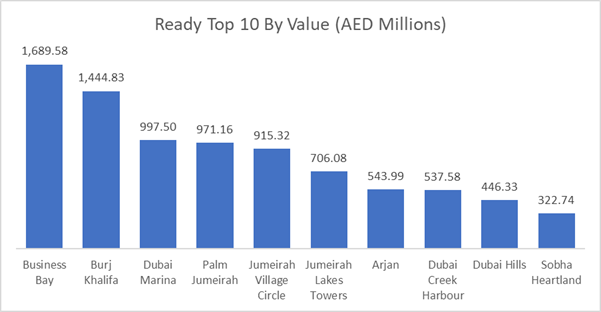

| Area | Value Traded (AED Billion) |

| Business Bay | 1.69 |

| Burj Khalifa | 1.44 |

| Dubai Marina | 1.00 |

| Palm Jumeirah | 0.97 |

| Jumeirah Village Circle | 0.92 |

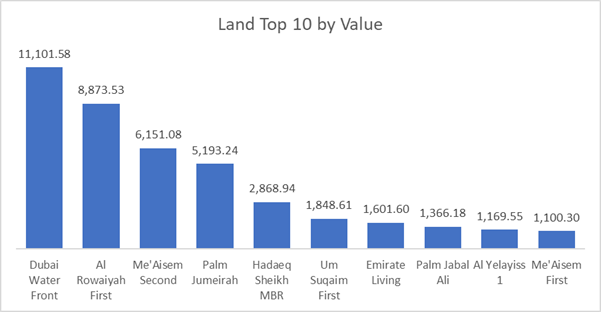

Land Market Performance

Total Land Value: AED58.70B (56.4% of the month)

Land didn’t just lead, it defined January. This is the core reason the overall month printed at AED104.09B and delivered the +92.5% YoY jump.

| Area | Value Traded (AED Bn) |

| Dubai Water Front | 11.10 |

| Al Rowaiyah First | 8.87 |

| Me’Aisem Second | 6.15 |

| Palm Jumeirah | 5.19 |

| Hadaeq Sheikh MBR | 2.87 |

Top Projects by Value Traded

Off-Plan (Top 10 Total: AED5.70B)

The top 10 off-plan projects collectively contributed ~19.4% of total off-plan value (AED5.70B out of AED29.35B), indicating a meaningful concentration in the biggest launches.

Top 3 by value:

- Nourelle — AED751.4M

- Lumena by Omniyat — AED682.1M

- Hado By Beyond — AED659.2M

Ready (Top 10 Total: AED1.56B)

The top 10 ready projects contributed ~9.7% of ready value (AED1.56B out of AED16.04B), implying ready demand is more distributed.

Top 3 by value:

- EOME — AED220.0M

- Bay Square — AED190.45M

- Sensoria at Five Luxe — AED179.67M

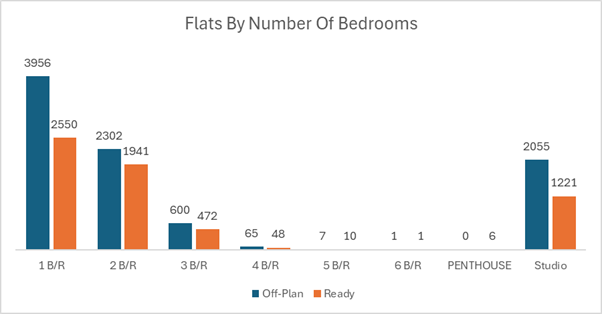

On The Micro Level

Flats are a 1BR + Studio market in both off-plan and ready, with ready showing a slightly stronger 2BR mix.

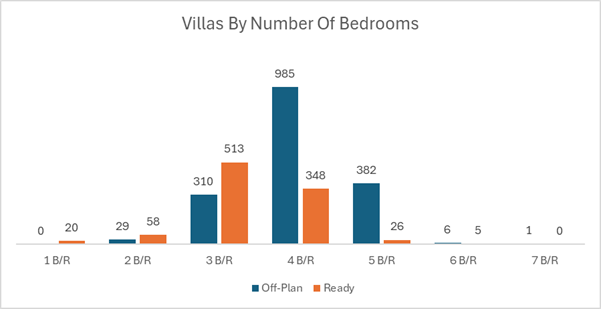

Off-plan villa demand is decisively family-upgrade (4–5BR), while ready is centered on 3–4BR liquidity.

Market Insights & Outlook

January 2026 printed an exceptional headline (AED104.09B, +92.5% YoY) primarily because Land dominated the value stack (56.4%), amplified by at least one ultra-ticket transaction. Underneath that, the built market stayed structurally consistent: flats led both off-plan and ready, with off-plan showing stronger recently launched concentration (top projects = ~19.4% of off-plan value) and ready reflecting broader distribution (top projects = ~9.7% of ready value). If land intensity normalizes in the following months, the key question becomes whether off-plan launch velocity (e.g., Damac Islands scale) can sustain overall market value at elevated levels without relying on land’s outsized contribution.